When does channel shift become cannibalization in gambling?

Tuesday 19 de March 2024 / 12:00

2 minutos de lectura

(United States).- With nothing less than the future of US igaming legislation at stake, the debate about whether visible online gaming cannibalizes landbased gaming revenue has further intensified. In a US context, we can only state one fact with certainty: nobody really knows the answer yet. However, we hope this blog will provide some useful international and economic context, as well as presenting some hypotheses and a ‘base case’ prediction of what the US can expect.

Inconspicuous consumption

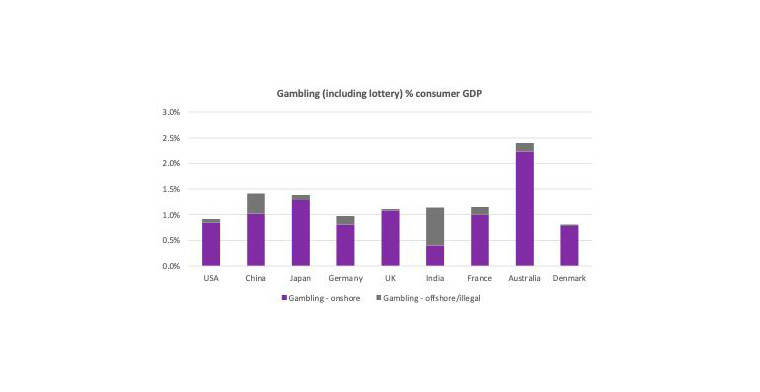

Due to regulatory and cultural differences, gambling markets look very different the world over. It is natural for most analysis to focus on the differences, especially where large black markets obscure underlying consumption patterns, However, a surprisingly consistent proportion of consumer GDP is dedicated to gambling regardless of regulation, culture, enforcement, and economic development. The chart below shows the G7 along with Australia as the outlier that proves the rule, and Denmark because we will be using long-term data from the Danish regulator.

There are broadly three tiers to the hierarchy of gambling expenditure globally:

- Big spending outliers: Australia, and (not on this chart) former constituents of the Ottoman Empire and its diaspora – from Greece to Georgia (we will be blogging on this curious anomaly soon)

- East Asian markets: which tend to spend between 1.0% and 1.5% of consumer GDP on gambling

- Everywhere else: which consistently tend to spend between 0.8% and 1.0% of consumer GDP on gambling

These bands are very sticky and so extremely important for working out cannibalization. If a gambling segment such as domestically regulated online gambling grows to become a significant part of a given gambling market, it can only do so either by displacing existing gambling expenditure (including black markets), or by growing the amount of money consumers spend on gambling at the expense of other non-gambling products and services. To state the obvious, the former is much easier to achieve and less dangerous from a policy perspective than the latter.

Online gaming expenditure per capita tends to settle at around US$50-150 when adjusted for consumer GDP, with those US states which have already legalized online gaming quickly setting the global record. US online gaming expenditure per capita might clear the US$200 level on some market projections, although we are conservatively capping it at US$165. On a consumer GDP adjusted basis, this means that regulated online gaming becomes c. 0.1% and 0.4% of GDP; with the USA already achieving the top end of this range where online gaming is allowed. In other words, for online gaming to be entirely incremental in the USA, it needs to grow existing gambling expenditure by fully 50%, taking its share of GDP from 0.8% to 1.2%. In other words, the USA needs to adopt a level of expenditure more similar to East Asian than Western markets. This level of consumer expenditure growth on gambling is entirely possible (as evidenced by the gaming-machine-driven Australian outlier), but we question whether it is likely or desirable.

Nevertheless, there is a middle-ground for the USA on this top-down basis. Most US states do not have a convenient and accessible means of gambling other than online sportsbook (limited by the volume and nature of US sports) and lottery (only high value scratch cards are fungible, but this is a c. US$9bn net revenue market, or c. US$30 per capita). Consequently, online gaming can reasonably take US expenditure from 0.8% to 1.0% of consumer GDP without stretching the economics of established consumer behaviour seen in comparable markets where landbased and/or online gaming is more accessible. However, 0.2% of consumer GDP growth only gets us to a per capita expenditure of c. US$90: and US igaming states are already materially outperforming that rate. Note, we believe that the black market being displaced is only worth c. US$25 per capita and this is already captured in our overall expenditure figures. Unlike in many other more open ‘grey’ markets (eg, Canada, Brazil, New Zealand), we do not believe that soaking up the existing black/grey market gets the USA very far.

The big channel shift problem the USA has compared to most other markets is that 77% of total existing consumer gambling expenditure is from landbased gaming and of this, 88% is from casino (commercial and tribal). If material igaming displacement has to come from somewhere, this is where it is going to come from. Whereas other jurisdictions have a number of sectors that can all suffer a little for online gaming growth, the USA is very casino driven. If channel shift becomes cannibalization in the USA, it is casinos that will inevitably suffer.

Is it okay if it’s just channel shift?

European gambling markets have adopted a digital euphemism for cannibalization that sounds far less dangerous: channel shift. From an economic perspective, channel shift has soporific frog-boiling characteristics which are easy to explain. Europe is different to the USA on many levels (which we discuss below), but one of the biggest differences is that a large number of European jurisdictions did not try to disrupt online gambling before they regulated it, unlike the USA with the (initially accidental) Wire Act, 1961, followed by (deliberate) UIGEA, 2006.

In the early 1990%, 100% of gaming was landbased by default. From launch in the mid-90s, online adoption growth by revenue was a fairly consistent 20% per annum, initially held back by such UX issues as dial-up internet and .com sites that wanted mostly to rip customers off (a revenue/deposits ratio above 65% was often considered a strong operating KPI rather than a sign of endemic fairness and safer gambling failings). However, the math(s) then becomes simple:

All we have assumed here is the following:

- Overall gaming grows with GDP (US GDP changes used)

- Online starts at 1% and grows at 20% pa until it reaches scale maturity in 2017, whereupon online growth slows to 10% pa

- Landbased gaming is the difference between the total and online growth

Crucially, for the first decade of channel shift, there is enough economic growth for landbased gaming to continue to grow. Then there is a recession which is a perfect excuse for landbased gaming not to grow. An economic bounce is then strong enough to lift both channels (read post pandemic), but this does not last long enough to protect landbased from the encroaching scale of online. This theoretical pattern is precisely what happened in Great Britain and Denmark from 2012 to 2023: online growth has been at the expense of absolute landbased decline, but this only started gradually at first and had some good regulatory excuses thrown in (eg, the loss of B2 content in the UK a year before the first lockdown).

In an organic adoption model, channel shift becomes more clearly cannibalization about half way through a generational shift, exacerbated by periods of economic disruption, high inflation, and regulatory change. Since Great Britain and Denmark have robust long-term data, we can see this simple theory working in practice in to different but similar Western markets.

After the 2009 global consumer recession, online betting was only c. 40% of total betting in these relatively betting-led jurisdictions (40% of online revenue vs. 20% for the US), while online gaming was only c. 25%. However, by 2023 channel shift has grown to c. 70% of betting and c. 50% of gaming.

- pre-pandemic, US disposable income reached US$16.6tr in Feb 2020, having grown at a relatively consistent 5% CAGR from 2013

- Disposable income increased to US$18.7tr in April 2020: 13% growth in just two months, with all landbased consumer activity heavily disrupted (ie, not just gaming)

- Disposable income hit a brief record high of US$21.9tr in March 2021, or 32% growth on pre-pandemic levels - more than six years of underlying economic growth had been given away to US consumers in just one twelve-month period

- While disposable income normalized to US$18.2k in May 2021, the stored-up consumer firepower going into 2022 was considerable

- Disposable income ended 2023 at US$20.6tr, implying 8% underlying CAGR since December 2019

Therefore, both exceptional policy and underlying economic drivers have been far more supportive of and disruptive to US disposable income growth 2019 to 2023 than the 5% CAGR seen pre-pandemic: this is the perfect storm of noise to hide underlying channel shift in. Essentially, if US consumer income continues to grow at 8% CAGR, then landbased gaming has nothing to fear as there is enough room for both online and landbased gaming to grow. However, this is a very big economic bet to take. In our view, overall growth of less than 5% CAGR is more likely than more than 5% for the next decade, albeit the USA will easily outperform most of big-state, low-productivity Europe.

We do not believe that any level of analysis can pick its way through these extreme levels macro and market noise to get to any robust position on the current state of channel shift in the USA.

The USA’s heavily gaming-led consumer preferences are also important for channel shift vs. many European markets. Landbased gaming has a structural benefit over betting in terms of channel shift which goes to the heart of our hypotheses developed below. For most consumers, betting is a brief, transactional experience which complements the enjoyment of a sporting event. Landbased betting venues outside stadia only add amenity when consumers bet over several events (eg, horseracing, encouraging dwell time), or want to bet with big screens, friends and potentially alcohol. Both the former latter consumer engagement drivers can be delivered in bars or at home with mobiles, meaning even the entertainment-led element of betting can be cannibalized by mobile, while the over-riding transaction-led element is far more efficiently delivered by mobile than by landbased POS (outside those wanting to transact anonymously and/or in cash). Betting therefore shifts to online early. Conversely, a mobile is a fiddly device to spend more than c. 15mins on at a time and less than five minutes per site for most consumer experiences is normal. A device designed for ‘snacking’ cannot compare to a large split-screen cabinet or a gaming table with a seat optimized for both rich game-play and comfortable dwell-time. Even if a gamer has no interest in playing with other people, eating in an in-house restaurant, or watching a show, landbased gaming is still a better experience than online. However, there will always be a critical mass of people who will take the benefit of not going anywhere vs. the amenity hit of mobile over casino. Mobile UX is also improving at a faster rate than slot machines and table games. If we assume that a critical mass of mobile gaming adopters are falling into two categories: younger mobile-first customers, and older but increasingly sedentary ‘sofa-first’ established players, then US casinos clearly have a double demographic problem that could lead to cannibalization.

Demand-driven cannibalization

Two of our hypotheses are demand-driven.

- As the aging population of the USA becomes even more sedentary, mobile forms of gambling will become increasingly popular at the expense of travel to casinos

- Younger customers are being trained to increase dwell-time on mobiles through social media and broader gaming experience, meaning their tolerance of an inferior product compared to landbased options is becoming higher (and technology improvements are closing the gap)

For the first, an older customer might continue to spend US$2,000 on gaming per year, but c. 33% of this might migrate online. In the short term, customers tend to increase their spend with new channels and then normalize it to what they can afford, creating the optical illusion of growth. However, this customer cohort is likely to be an overall growth segment for US online gaming because of the inefficiency of existing landbased gaming supply: hence omnichannel customers becoming worth a lot more than solus customers, because they can gamble whenever they want. Allowing online gaming therefore supports overall gaming expenditure from this cohort and mitigates behavioural decline: this is more channel shift than cannibalization, albeit the two could look very similar and a freely accessible high quality mobile offer might accelerate an otherwise structural decline in venue visits.

The younger customer cohort looks like an engagement opportunity at first: younger, more middle class, less likely to go to a landbased venue and so incremental revenue that is otherwise very hard to tap outside occasional visits to Las Vegas. However, this is the frog-boiling cohort. In the 1990s and before, all these customers either gambled in a landbased venue or did not gamble at all. Currently, a small proportion use black markets or social gaming. An online offer allows them to miss landbased out completely, narrowing the landbased cohort into a socio-economic timebomb of existing older, less well-off adopters. Cannibalization is often generational: slow, imperceptible at first, but remorseless and leading to absolute decline when a tipping point is reached.

Supply-driven cannibalization

Supply-driven choices can either exacerbate or mitigate these demand-driven drivers of channel shift.

- Venues which optimize monetizing older, ‘transactional’ customers will accelerate channel shift

- Venues which optimize the community and entertainment characteristics of landbased gaming can create an omnichannel win-win with the right operations management

These hypotheses are not new: your author has been espousing them since 2003, but the ‘transactional gaming customer’ proved far more resistant to change than a young analyst imagined (demonstrating a greater aptitude for strategy than stock picking before gambling businesses uniformly failed to spot a global regulatory storm coming). However, the problems of a customer cohort introduced to 5-reel multi-line slots in the 1970s are now becoming actuarial in form and substance. Tired offers built around customers who are principally there to transact are ripe for disruption if online gaming is allowed and expanded: a slow death will be accelerated through cannibalization.

Note, we have not attempted to estimate the non-gaming revenue of Tribal venues in the chart above; this is a Commercial figure only

However, entertainment-led landbased offers can always give something that remote channels cannot and probably never can: transact at home; be entertained in venue is a solid brand-building omnichannel strategy with decades to run, in our view. We believe that non-gaming revenue is a reasonable proxy for the entertainment utility of gaming venues. Our very broad rule of thumb is that a non-gaming revenue of less than 20% probably puts the overall offer into the at-risk ‘transact’ category, while above 20% puts it in the more robust ‘entertain’ segment. Tellingly, we believe there is only one casino in Great Britain that is in the ‘entertain’ category by this measure, and it is the only one which has delivered consistent growth despite being constrained in its slot offer.

Not all Winners or Entertaining Change?

We believe that our top-down, bottom-up and behavioural economics hypotheses can be neatly triangulated into a base case of what happens if or when online gaming becomes more prevalent in the USA through legalization:

- About US$90 per capita can be found by improving utility compared to an inefficient supply of lanbased gaming venues, although there are big variations by state

- About US$30 per capita will come from illegal supply and disrupting high value slots

- Up to US$100 per capita will come from landbased gaming venues with tired or limited consumer propositions, which is up to 33% of total supply across the USA, including Las Vegas

Landbased casinos can still thrive in this context, but only if they provide venues that give customers reasons to turn up based on something more solidly regenerative than new slots and old habits. We would estimate that more than 50% of US casinos are currently failing in that mission, but that still implies a much more resilient and attractive landbased gaming sector than found across most of Europe.

Equally, Europe has demonstrated very clearly that the fast-paced digital-led operations management needed to gain scale in online gambling is not just alien to but cross-grained with the compliance-driven command-and-control bureaucracies favoured by most landbased gaming companies (note, being compliance-driven rarely creates genuinely compliant businesses, just risk-averse ones). The most boring landbased venue concepts are also typically the product of conservative middle-management committees.

Digital channel shift is inevitable, and a degree of cannibalization will become a fact of life at least to some degree in the US wherever igaming gains traction. Igaming is already too strong in the markets where it has been allowed not to be disruptive. However, this only needs to be a cannibalization disaster for those landbased companies and venues who are already taking their customers for granted, or who fail to adapt their management style to optimizing omnichannel opportunities.

Categoría:Reports & Data

Tags: Sin tags

País: United States

Región: North America

Event

SiGMA Central Europe

03 de November 2025

SiGMA Central Europe 2025 Closes First Edition with High Attendance and Roman-Inspired Experiences

(Rome, Exclusive SoloAzar) - The first edition of SiGMA Central Europe in Rome came to a close, leaving a strong impression on the iGaming industry. With thousands of attendees, six pavilions brimming with innovation, and an atmosphere that paid homage to Roman history, the event combined spectacle, networking, and business opportunities. It also yielded key lessons for future editions.

Friday 07 Nov 2025 / 12:00

Innovation, Investment, and AI Take Center Stage on Day 3 of SiGMA Central Europe

(Rome, SoloAzar Exclusive).- November 6 marks the final and most dynamic day of SiGMA Central Europe 2025, with a packed agenda that blends cutting-edge tech, startup energy, and investor engagement. With exhibitions, conferences, and networking opportunities running throughout the day, Day 3 promises to close the event on a high note.

Thursday 06 Nov 2025 / 12:00

SiGMA Central Europe Awards 2025: BetConstruct Wins Innovative Sportsbook Solution of the Year

(Malta).- BetConstruct has been recognised at the SiGMA Central Europe Awards 2025, receiving the Innovative Sportsbook Solution of the Year award. This achievement highlights the company’s continued focus on elevating retail betting experiences and supporting operators with solutions that create measurable business value.

Wednesday 05 Nov 2025 / 12:00

SUSCRIBIRSE

Para suscribirse a nuestro newsletter, complete sus datos

Reciba todo el contenido más reciente en su correo electrónico varias veces al mes.